This post was initially published at Debtwire.com

A Florida-based senior living project with a technical default and a chunk of subordinate bonds that are valued higher than the senior debt illustrates the sometimes-opaque nature of municipal bond pricing, several market participants say.

Florida-based conduit issuer Capital Trust Agency in June 2018 issued USD 81.97m in senior living revenue bonds on behalf of H-Bay Ministries, Inc.’s Superior Residences Project. Bond proceeds were used to acquire five stand-alone assisted living and memory care properties in Hillsborough, Lake, Citrus, Okaloosa and Marion Counties in Florida, consisting of 340 rental assisted living and memory care units.

The bonds were issued with senior and subordinate liens – the USD 39.68m Series 2018A-1 senior living revenue bonds, the USD 13.34m taxable Series 2018A-2 senior living revenue bonds, the USD 20.235m second tier Series 2018B senior living revenue bonds and USD 8.72m third tier Series 2018C senior living revenue bonds.

The bond trustee, Wilmington Trust, National Association was notified of default on 29 May, and filed a notice of default on 12 June after the borrower failed to comply with a debt service coverage ratio (DSCR) covenant test in FY19. The trustee may now accelerate the bonds and/or foreclose on the project, and holders have been asked to vote on a course of action.

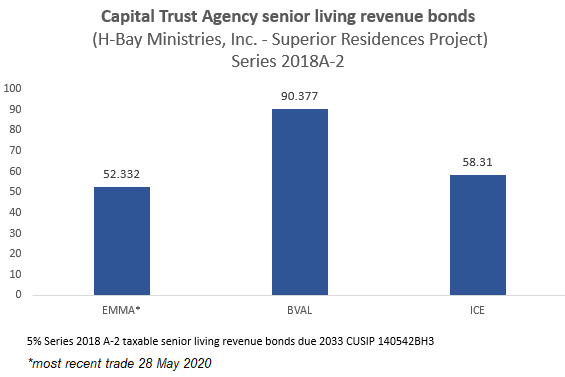

Like many senior living projects, H-Bay Ministries has been hit hard by the coronavirus (COVID-19) pandemic. Despite the distress and a technical default, the bond evaluations show how difficult it can be to accurately value bonds when there is little trading, as is common in the high yield muni market. The subordinate Series C bonds are actually valued higher than the senior bonds, which are also valued significantly higher than recent trading prices shown on Electronic Municipal Market Access (EMMA).

A quote from Intercontinental Exchange (ICE) for the most subordinate bonds of a defaulted credit is 27.447 points higher than the most recent EMMA trade of the most senior bonds.

There is a potential justification for marking the subordinate bonds higher – but it’s a weak argument, a portfolio manager said.

“Some of these are underwritten so when there’s a default, the collateral (could) become pari passu as opposed to senior and subordinate bonds,” the portfolio manager said. “But if you’ve gotten to a point where you’re thinking about liquidating collateral, they should be worth the same amount, because of a pro-rata amount of liquidated collateral (as outlined in the official statement).”

Regardless, the subordinate bonds “shouldn’t be marked higher” than the seniors, the portfolio manager said.

S&P Global Ratings has downgraded the project twice since 3 April, including yesterday (23 June) to B+/negative for the Series 2018A-1 and taxable Series 2018A-2. The Series 2018B bonds were downgraded to B-/negative. In April, S&P downgraded the Series 2018A-1 and Series 2018A-2 bonds to BB/negative from BBB, and the Series 2018B bonds to B/negative from BBB-, citing management concerns and COVID-19. S&P also downgraded three other affiliated projects affiliated with the borrower on 3 April, and a fourth, which defaulted in February, is now rated at D.

Price check

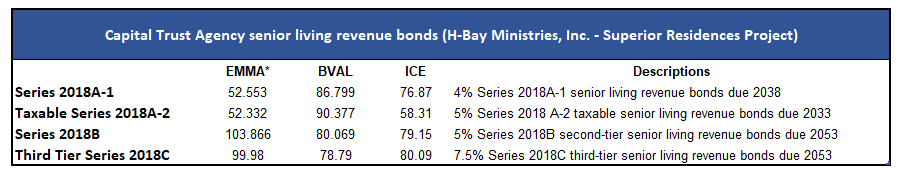

A 2038 maturity of the Series 2018A bonds priced at 52.553 when it last traded on 1 June, according to EMMA. On 22 June, ICE provided a quote of 76.87, and BVAL quoted a price of 86.799 – 24.317 and 34.246 points higher than the most recent trades on EMMA, respectively.

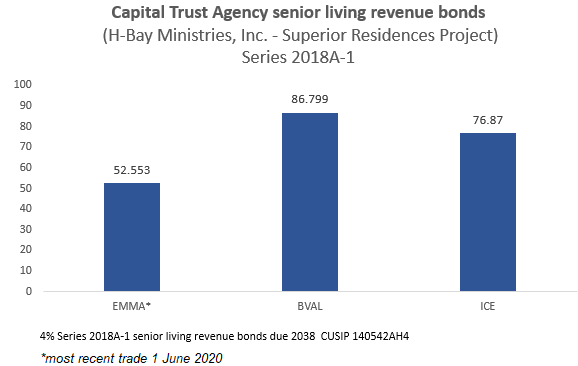

Meanwhile, a 2033 maturity of the Series 2018A-2 taxable bonds last traded at 52.332 on 28 May, according to EMMA. ICE quoted a price of 58.31 for those bonds, and BVAL quoted 90.377 on 22 June.

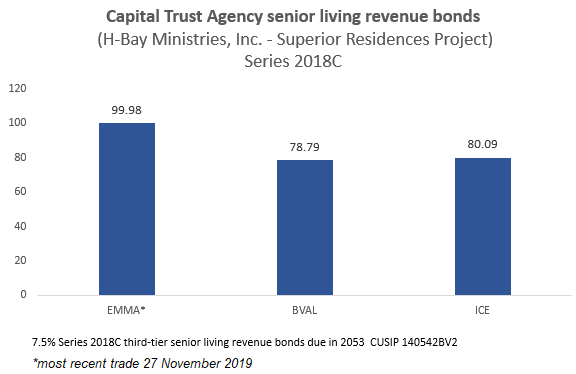

The most subordinate debt, the Series 2018C bonds haven’t traded since 2019, when they were priced at 99.98. ICE quoted 80.09 and BVAL quoted 78.79 on 22 June.

In fact, a 2053 maturity of the Series 2018A-1 bonds hasn’t traded in the 80s since March, according to EMMA. The last recorded trade was 17 June at 55.95. ICE values that maturity at 67.48.

“Typically if the A bonds are not getting par, the B bonds and C bonds are getting wiped out,” the second portfolio manager said. “I find the lack of guidance and subjectivity with regard to pricing high yield munis is problematic.”

A third portfolio manager reviewed the suggested pricing and said it was “unusual,” and an analyst familiar with the credit said that the pattern is an “anomaly.”

Institutional holders may not want to sell at 60 to keep the value of the portfolio artificially inflated, the second portfolio manager said. They then make the argument to pricing services that there haven’t been enough trades on the bonds to warrant the lower price and threaten to pull business if they aren’t appeased.

“They’re pricing for institutions, and then what about the retail world? You’re lying, and telling the retail world they’re worth 75, and when you put out for a bid, you get a 57 bid, not 75, and the broker isn’t going to have an answer,” the second portfolio manager said. “I think it’s a problem. How many trades does it take for them to adjust the price? That’s a problem. And the retail world, even high yield munis, in default, expect a much slower bid than what your account statement says – it’s not a real indicator of what the bonds are worth.”

Representatives from ICE and BVAL declined to comment for this report.

“Pricing services are getting paid to accurately reflect the pricing … and it’s misleading,” the second portfolio manager said. “People get their statements, and (say the asset values) are doing OK, because it’ll say the bond’s worth 86. But if you put it out for bid, the junior subordinated bonds should be much lower. If the As are in the 50s following a default, then the Bs should be in the 20s and the Cs should be behind both.”

‘There’s default and then there’s default’

A default from a covenant miss is a different default than one stemming from non-payment, said the analyst familiar with the credit. At Superior Residences and the affiliated properties with municipal debt, holders have been concerned about volatility in management and leadership since last year, they said.

Superior Residences’ default stemmed from a missed DSCR covenant test; it reported 0.94x, compared to a 1.05x requirement, according to the analyst.

“I don’t think anything is happening, it seems like they’re still paying on these bonds,” the analyst said.

In 1Q20, total revenues were USD 4.3m, 0.46% below budget, according to a disclosure. Average occupancy totaled 86%, with 293 units occupied. Operating expenses totaled 4.57m, or 2.4% above budget. Superior Residences reported a negative net income of USD 271,971 in 1Q20, and noted that the DSCR was below 1.05x. COVID-19 didn’t begin to have an impact on the portfolio until the middle of the quarter. The fiscal year begins 1 January.

The facilities need to reach 90% to 92% occupancy to break even, said Seth Walker, CFO of SRI Management, the facility’s management company during an investor call 27 May. Occupancy in 1Q20 was 86%.

by Maria Amante, Caitlin Devitt and Kathie O’Donnell